Social Security Claiming Strategies for Single, Divorced & Widowed Women

By Scott Tschappat

It may not come as a surprise to hear that women face more retirement challenges than men due to lower wages and time off work to care for children. In addition to that, being a single woman without a partner adds another layer of complexity to the situation.

Due to factors such as longer life expectancy, lower marriage rates and high divorce rates, it is projected that most women will end up alone. Therefore, it is crucial for women to take charge of their financial lives. Even if you have saved for retirement, it’s important not to overlook your Social Security benefits. They belong to you and taking the time to utilize them based on your circumstances will support financial well-being in the long run. Read the following tips from our team to understand how you can best prepare yourself and your financial future.

For the Single Women

Many women make the mistake of claiming Social Security as soon as they’re eligible. Few wait until full retirement age, and even fewer wait until age 70. But your benefit amount increases by 8% each year from 66 to 70, plus cost of living increases for inflation, so it pays to wait.

For example, let’s say your full retirement age is 66 and your monthly payment is estimated to be $2,000. The chart below shows how much you’d get every month if you started collecting at age 62 (reduced benefits), 66 (full benefits), and 70 (increased benefits).

Just by waiting until age 70, your monthly payout increases substantially, which could lead to thousands of more dollars throughout your retirement for you to invest or gift to others.

But when you should claim benefits isn’t as simple as waiting until age 70. Your health, home, and personal circumstances could indicate otherwise. Maybe you find out you have advanced-stage breast cancer, so you start taking benefits at age 62. Or maybe you are in good health and since you have plenty of other resources, so you wait until age 70. Tailoring your claiming strategy to your unique life circumstances is key, and a professional can help you take all factors into account.

For Those Who Are Divorced

This may come as a surprise, but divorcées can claim their ex-spouse’s benefits as long as they were married for at least 10 years. The amount you receive is equal to 50% of your ex’s benefits. If you qualify for your own benefits, you either receive 100% of your benefit amount or 50% of your ex’s, whichever is higher. The best part? Your ex never has to know you’re collecting spousal benefits. Social Security doesn’t notify them and you’re not required to reach out.

If your ex passes away, you receive benefits as a widow, which means you get 100% of your ex’s payout. There is one caveat to this rule, however. You won’t qualify for spousal benefits if you remarry. Your ex can, but you can’t. Although, if you happen to remarry and your second marriage ends in divorce or your spouse dies, you’d once again be eligible for your first spouse’s benefits.

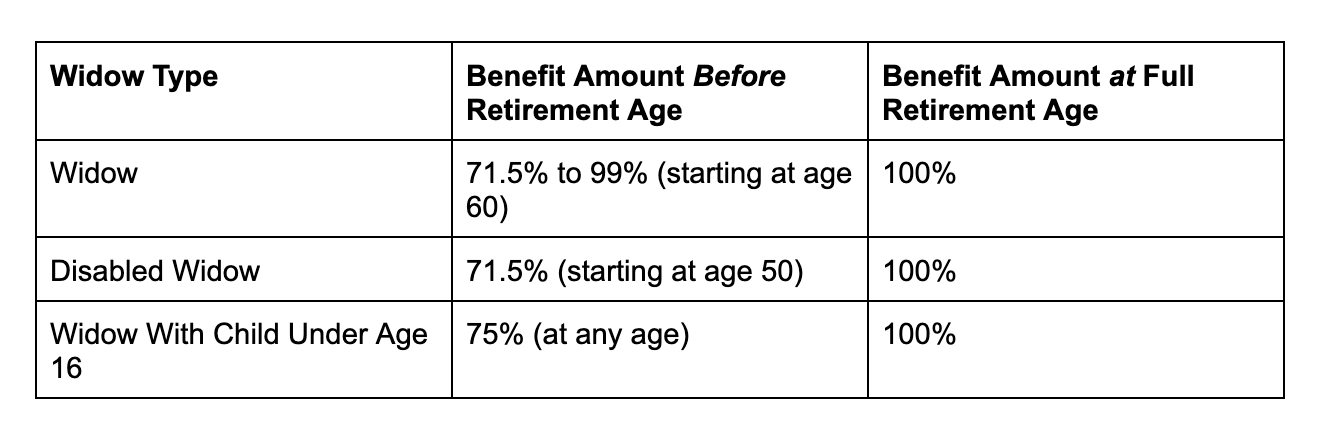

For the Widows

Widows and divorcées who were married for at least a decade are eligible for survivor benefits when a spouse dies. Just keep in mind that you won’t qualify for survivor benefits if you remarry before age 60.

As with regular Social Security payouts, you receive reduced benefits if you claim them before you reach full retirement age. But unlike regular payouts, you don’t have to wait until you’re 70 to get the highest amount.

The chart below shows what percentage of survivor benefits you’d get based on your situation:

Lean On Your Trusted Professional

Social Security can be a complex maze to navigate, and it may be helpful to work with a financial professional to gain clarity while potentially increasing your benefits. At Acute WealthCare, we offer personalized support to help you evaluate your options and choose a claiming strategy that fits your situation. We are here to guide you through Social Security and the unique challenges you may face as a single woman. Schedule a 15-minute introductory phone call to get the support you need.

About Scott

Scott Tschappat is a wealth advisor at Acute WealthCare, an independent, fee-based comprehensive financial services firm with over 20 years of experience. Scott is committed to helping his healthcare worker clients create a financial plan that brings them comfort and dignity. Scott learned the importance of proper financial management and making a plan for the unexpected at a young age when his father passed away suddenly and he watched his mother use the life insurance money wisely to take care of their needs, both present and future. He strives to steward his clients’ money well, as if it were his own mother’s, and help them every step on the journey to their financial future.

Scott lives in Highlands Ranch, CO, with his wife, Bridget, a school counselor at All Souls Catholic School, and their two daughters, Sarah and Emily. He loves sports and has been lucky enough to coach both of his daughters’ basketball teams. In the spring and summer, you can find Scott getting his hands dirty gardening and enjoying live music at Red Rocks or another local venue. To learn more about Scott, connect with him on LinkedIn. You can also register for his latest webinar on What We Do & How We Help.